》Check SMM Copper Quotes, Data, and Market Analysis

》Subscribe to View SMM Historical Spot Metal Prices

》Click to Access the SMM Copper Industry Chain Database

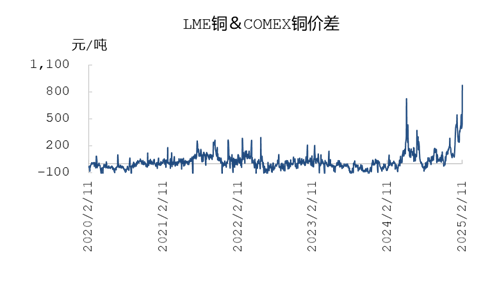

From January 2 to February 11, 2025, the two-week closing price increases for LME and SHFE copper were approximately 6.316% and 5.28%, respectively. Compared to the two-week increases of around 6% and 5% for LME and SHFE copper, it is noteworthy that the COMEX most-traded copper contract surged by over 11% to 15.26%, significantly outperforming the SHFE most-traded contract and the LME 3M copper contract. Since May 2024, the price spread between the COMEX most-traded contract and the LME 3M contract has widened again, reaching nearly $950/mt during intraday trading on February 11, 2025. Unlike the short squeeze scenario on COMEX in 2024, this time the price spread window has lasted longer and exhibited greater volatility. Below is a detailed analysis.

From the perspective of inventory, the widening price spread between COMEX and LME this time was not caused by a short squeeze. Since May 2024, COMEX copper cathode inventories have been steadily increasing, currently reaching nearly 90,000 mt, a six-year high. The primary reason lies in the frequent adjustments to tariff policies by the Trump administration since January 2025, which involved imposing or threatening to impose additional tariffs on multiple countries, including Mexico, Canada, China, and Europe. On January 20, a 25% tariff on Mexico was announced, accompanied by an executive order to strengthen import controls. Subsequently, there were threats to impose tariffs on the EU and plans to impose tariffs on Mexican goods, while tariff implementation on Canada was delayed. In early February, the exemption for small-scale trade tariffs with China was withdrawn, and on February 10, a 25% tariff on aluminum products was announced. The overall tariff policy remains uncertain, exacerbating global trade tensions.

Initially, the repeated announcements of hefty tariffs on goods from Canada, Mexico, and China by the Trump administration, followed by delays in implementation, caused market expectations to fluctuate sharply. This policy uncertainty prompted US market participants to price in potentially higher future import costs, driving COMEX copper prices significantly higher.

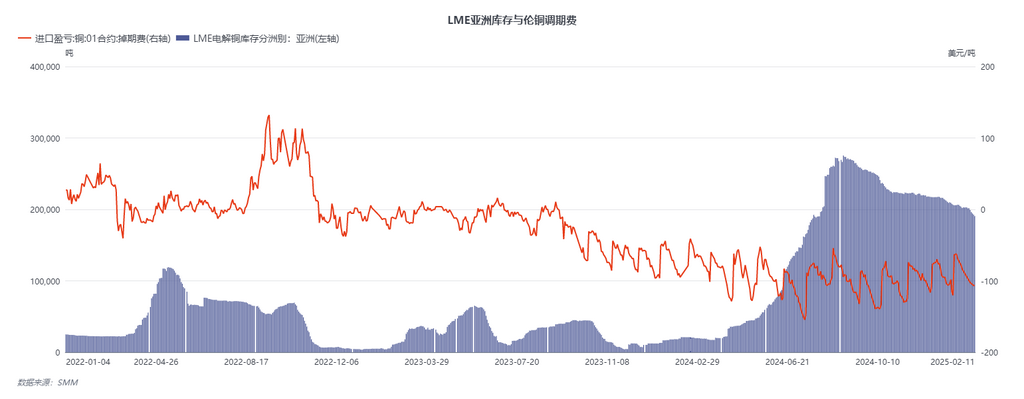

Secondly, structural changes on the supply side also played a key role. Domestic copper cathode supply in the US is constrained, with imports heavily reliant on Chile, Canada, Peru, and Mexico. In 2024, these four countries accounted for nearly 90% of imports, while China and Europe accounted for only 0.1%-0.2%. In contrast, the Asian and European markets have relatively ample supply, creating a clear market divergence and arbitrage opportunities. Lastly, arbitrage trading and capital effects were amplified during this process, with arbitrage funds actively exploiting the premium differences between the two markets, further driving up COMEX copper futures prices. These factors collectively contributed to the widening LC price spread between LME and COMEX.

As a result, the international trade flow of copper cathode has undergone the following changes since January 2025: First, deliverable copper cathode in LME Asian warehouses that can be shipped to COMEX has been continuously cancelled, with cancelled warrants being shipped to North America starting in January. Second, shipments from South America to Asia have decreased, with some long-haul shipments being delayed. According to market sources, some primary long-term contract issuers have reduced shipments to China. Third, during the Chinese New Year, some African-origin cargoes were also shipped to North America. Currently, it is estimated that the volume en route to North America is between 55,000 and 65,000 mt.

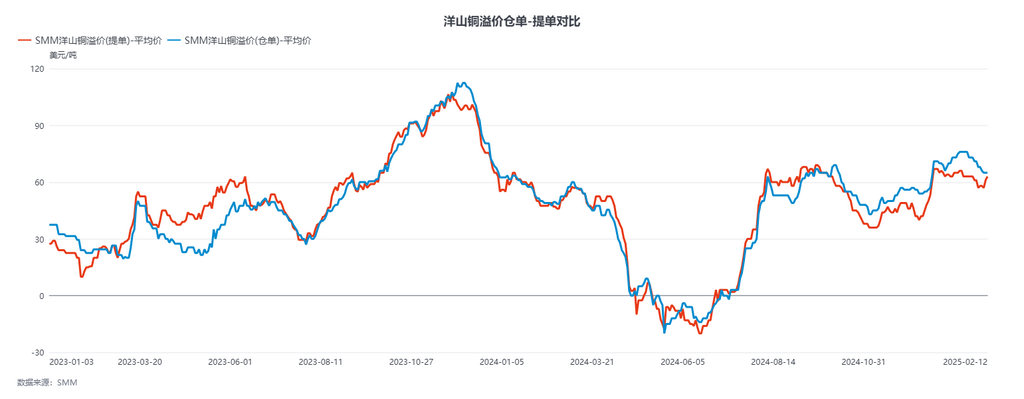

Looking ahead, the sustained opening of the LC price spread window may have the following impacts: First, due to active cross-market arbitrage activities, a significant inflow of arbitrage funds into the US market is expected to drive a notable increase in US imported copper volumes. Meanwhile, China's import volume is expected to decrease relatively, particularly for registered cargoes from South America. This arbitrage behavior is prompting large traders and smelters to reconfigure logistics channels. Given the uncertainty surrounding US tariff policies, the reduced import volume from February to April is expected to support Yangshan copper premiums.

Driven by arbitrage funds and rising expectations of higher import costs in the US market, the price advantage of imported copper in the US is expected to become more apparent. Trade ties between the Americas and the Asia-Pacific region, after a short-term surge, are likely to gradually weaken, further exacerbating the fragmentation of global trade structures.

Secondly, the continued cancellation of warrants in LME Asian warehouses is expected to lead to a sustained decline in LME inventories, thereby narrowing the contango structure of LME copper. This implies that future arbitrage opportunities based on high spot-futures price spreads will correspondingly decrease, pushing up the holding costs of US dollar-denominated copper and weakening the driving force for cross-market arbitrage, while increasing CIF B/L premiums. Finally, due to the sustained high COMEX copper prices and the anticipated Chinese countermeasures against US tariffs, Chinese companies, particularly traditional copper scrap importers using COMEX contracts, are expected to significantly reduce copper scrap imports from the US. This will directly tighten domestic copper raw material supply, intensifying the balance pressure of copper elements in the domestic market. During a period of tight copper concentrate TC, the decline in copper scrap import volumes may continue to push up production costs for downstream smelters, keeping domestic market prices well-supported under tight supply conditions.

![The Most-Traded BC Copper Contract Closed Up 1.68%, Easing Conflict Boosted Copper Prices [SMM BC Copper Commentary]](https://imgqn.smm.cn/usercenter/kvwSZ20251217171710.jpg)